Quest for Yield series (1)

China Taiping's i-Save June 2020 tranche

In my recent quest for yield, I came across China Taiping's i-Save 2.05% p.a. 3-year term endowment. This June 2020 tranche is a single premium plan that is both capital and yield guaranteed, provided it is held till maturity.

"What? Are you sure such a decent interest rate still exists?", you asked.

Yes, let's look at the details.

How safe are my hard-earned savings?

"My premium is guaranteed by who?" The insurer themselves, China Taiping Insurance (Singapore) Pte. Ltd. ("CTIS"). Eh say what!? Ownself guarantee ownself*? Zhun bo*?

*Singlish. For more information, Google online or refer to this opinion piece from New York Times

In such a circumstance, the onus is on us to conduct due diligence on the company providing the guarantee and assess how comfortable we are with the information found.

We are largely familiar with insurers such as NTUC, Prudential, AIA, Aviva etc. So what's with this CTIS? How reliable are they since I have not heard of them before?

CTIS - Know Your Guarantor

The company originated from Tai Ping Insurance Co. Ltd Singapore Branch, which was established in Singapore since 1938. Based on the Monetary Authority of Singapore's ("MAS") website, CTIS holds a Direct Insurer (Composite) license in Singapore. It apparently received its license in August of 2018 and is one of 8 composite insurers.

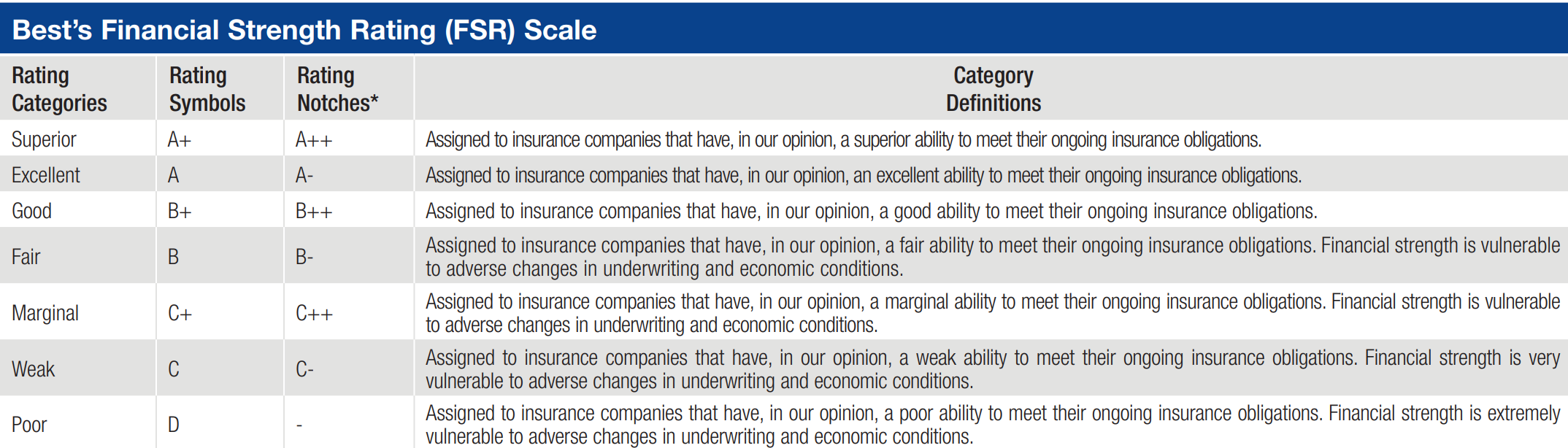

According to the company's website, its Financial Strength is rated A- by S&P and A by A.M. Best, a U.S.-based credit rating agency that focuses on the insurance industry. No further information can be found on its S&P credit rating. Referencing from a Bloomberg article dated 28 June 2019, A.M. Best affirmed the Financial Strength Rating ("FSR") of A (Excellent) and the Long-Term Issuer Credit Rating ("ICR") of a for CTIS.

What do these grades mean?

FSR -

A.M. Best defines FSR as "an independent opinion of an insurer's financial strength and ability to meet its ongoing insurance policy and contract obligations".

An FSR is "not a recommendation to purchase, hold or terminate any insurance policy, contract or any other financial obligation issued by an insurer..".

Source: A.M. Best

ICR -

A.M. Best defines ICR as "an independent opinion of an entity's ability to meet its ongoing financial obligations and can be issued on either a long- or short-term basis. A Long-Term ICR is an opinion of an entity's ability to meet its ongoing senior financial obligations, while a Short-Term ICR is an opinion of an entity's ability to meet its ongoing financial obligations with original maturities generally less than one year. An ICR is an opinion regarding the relative future credit risk of an entity. Credit risk is the risk that an entity may not meet its contractual financial obligations as they come due. An ICR does not address any other risk.".

In addition, an ICR is "not a recommendation to buy, sell or hold any securities, contracts or any other financial obligations..".

Okay, okay, enough of the broken recorder. I know and understand that the risk is mine to take.

Source: A.M. Best

CTIS is wholly-owned by China Taiping Insurance Holdings Company Limited ("CTIHC"), a Chinese insurance conglomerate listed on the Hong Kong Stock Exchange since 2000. CTIHC is owned (59.64% as of 31-Dec-2018) by China Taiping Insurance Group Limited ("CTIGL") which is held by the Ministry of Finance of the People's Republic of China (90%) and the National Social Security Fund (10% as of January 2019).

As of 16 March 2020, Fitch has affirmed the Issuer Default Ratings ("IDR") on CTIHC and CTIGL at A (Strong).

Fitch -

Per Fitch, "IDRs opine on an entity's relative vulnerability to default (including by way of a distressed debt exchange) on financial obligations. The threshold default risk addressed by the IDR is generally that of the financial obligations whose non-payment would best reflect the uncured failure of that entity. As such, IDRs also address relative vulnerability to bankruptcy, administrative receivership or similar concepts. In aggregate, IDRs provide an ordinal ranking of issuers based on the agency's view of their relative vulnerability to default, rather than a prediction of a specific percentage likelihood of default."

Source: Fitch

Came across Uncle CW's post recently on SMOL's often quoted "Trust But Verify". Aside the Big 4, how applicable is it to credit rating agencies? Have you watched the Big Short? Here's a short scene.

Source: Youtube

"What if Great Financial Crisis happens again?"

Policy Owners' Protection Scheme

Insurers licensed in Singapore are supervised by the MAS. In the worst case scenario, the second layer of guarantee comes from the Policy Owners' Protection ("PPF") Scheme which protects policy owners in the event of a failure of a life or general insurer which is a PPF Scheme member. CTIS is a Scheme Member.

This Scheme provides 100% protection for the guaranteed benefits of your life insurance policies, subject to caps where applicable. For example, for individual life and voluntary group life policies, there are aggregate caps applicable, namely SGD500,000 for the guaranteed sum assured and SGD100,000 for the guaranteed surrender value per life assured per insurer.

How does this endowment work?

Let's recall. This single premium plan provides a guaranteed return of 2.05% p.a. only if it is held for the full 3 years.

The yield definitely caught my attention in this low environment of interest rates where Banks are lowering their deposit rates left right and centre with the most recent by CIMB Singapore. Its Fastsaver and Starsaver rates are being revised down by 50% off the first-tier of retail deposits respectively. How do you foresee the rates will be going forward?

What happens if I will to surrender before the 3 years are up? What happens if something happens along the way? Let's look at the product illustration for this June 2020 tranche of i-Saver.

Source: CTIS

From my interpretation, which seems to make the most sense for now (correct me if not the case..), the guaranteed Surrender Value after inception and till end of policy year 1 is 90%, after year 1 till end of policy year 2 is 95% and after year 2 till before policy matures at the 3 year mark is 97.5%.

Ouch! Quite harsh I must say for the penalty if we do not hold till maturity. Hence, please only consider this product if you really do not see the need for the use of funds for the next 3 years.

On the bright side, if we managed to hold till maturity, the interest earned each year will be compounded at 2.05% and guaranteed at the end of 3 years. Also, the plan includes a guaranteed 105% of premium as Death benefit cover from the second year.

Here's some other noteworthy mentions:

- the minimum premium size is SGD30,000

- insured from ages of 1 to 18 age next birthday can apply with their parents as policyholder and themselves as life assured.

- not able to purchase using SRS funds.

How do I subscribe to this single premium plan?

From the company's website, CTIS i-Save seems to be only available through their distribution channels. Its partners include ICBC and several Financial Advisory firms. ICBC has about nine branches all over Singapore. We can walk in to the Bank or contact a FA.

If you wish to sign up for it online, it seems that InsureDIY is the only platform offering CTIS's i-Save with an online process. The company is licensed as an Exempt Financial Adviser.

The experience of online purchase is so-so at best and I have had better. It definitely has room for improvement such as stating the format of files that can be uploaded. The platform is not explicit in that one can only use image types for your upload of ID. Additionally, a potential subscriber is still able to upload in other extensions such as pdf, word etc and will not be auto-prompt for gif, jpg, png etc. Please note that only the latter types of extension are applicable. The other part is the signature section. Quite a hassle.

However, the comparison is not apple-to-apple since this is a third-party platform and I have not been through numerous online sign-ups yet. At least I do not need to set appointments and make a trip out in this current Phase 2 situation. It can be done at my own pace and comfort but there will be no one to serve me. For the same distribution cost, you may prefer the human touch to it - you can socialise and at the same time enjoy the services provided by ICBC/ FA.

*Disclaimer: At no cost to you, you may wish to consider using my referral link here and referral code - moo041 if you opt to sign up online. In fact, both you and I will be equally rewarded with DIY$10 :)

Comments

Post a Comment